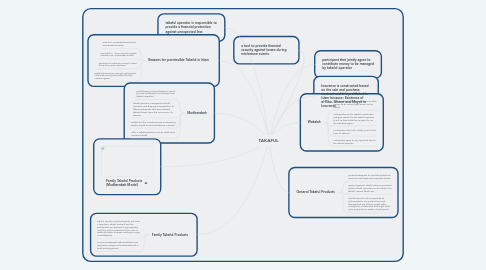

1. a tool to provide financial security against losses during misfortune events

2. takaful operator is responsible to provide a financial protection against unexpected loss

3. Reasons for permissible Takaful in Islam

3.1. Free from unjustified enrichment, uncertainty and Riba.

3.2. Operated in two common models; Wakalah and Mudharabah model.

3.3. participant contribute money to assist those who need assistance.

3.4. Replaced insurance concept- participants cooperate among themselves for their common good.

4. Mudharabah

4.1. profit sharing contract between capital provider (partcipant) and entrepreneur (takaful operator).

4.2. Takaful operator manages the takaful operation and they pay compensation to fellow participants who have suffered defined losses upon the occurrence of a disaster.

4.3. Profits from the investment and underwriting surplus should be shared between 2 parties.

4.4. offer 2 Takaful products; Family Takaful and General Takaful.

5. Family Takaful Products (Mudharabah Model)

6. Family Takaful Products

6.1. Takaful operator and participants will enter a long term Takaful contract and the participants are required to pay regularly and they will be protected in the case of death and other mishaps resulting in injury or disablement

6.2. Provide participants with protections and long term savings and investments with a fixed maturity period.

7. participant that jointly agree to contribute money to be managed by takaful operator

8. Insurance is constructed based on the sale and purchase contract and it is prohibited in Islam because: Existence of al-Riba, Gharar and Maysir in Insurance

9. Wakalah

9.1. contract where a person authorizes another person to do certain legal action on his behalf.

9.2. Participants pay the Takaful contribution and give consent to the Takaful operator to act on their behalf as an agent to run the Takaful program.

9.3. contributions flow into Takaful pool on the basis of Tabarru’.

9.4. Participants agree to pay specified fees to the Takaful operator

10. General Takaful Products

10.1. products designed to meet the protection needs of individuals and corporate bodies.

10.2. Types of general Takaful schemes provided by the Takaful operators: motor takaful, fire takaful, marine takaful etc.

10.3. Takaful operator will compensate its participants for any material loss and damage that any of them might suffer arising from a misfortune that might inflict upon properties or assets of participants.