Unlock the full potential of your projects.

Try MeisterTask for free.

¿No tienes una cuenta?

Regístrate Gratis

Navegar

Mapas Destacados

Categorías

Gestión de proyectos

Objetivos de negocio

Recursos humanos

Lluvia de ideas y análisis

Marketing y contenido

Educación y notas

Entretenimento

Vida

Tecnología

Diseño

Resúmenes

Otros

Idiomas

English

Deutsch

Français

Español

Português

Nederlands

Dansk

Русский

日本語

Italiano

简体中文

한국어

Otros

Ver mapa completo

Copiar y editar mapa

Copiar

Insurance

Objetivos de negocio

LA

Laura Alfano

Seguir

Comienza Ya.

Es Gratis

Regístrate con Google

ó

regístrate

con tu dirección de correo electrónico

Mapas Mentales Similares

Esbozo del Mapa Mental

Insurance

por

Laura Alfano

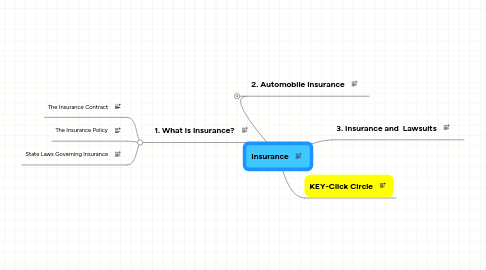

1. 1. What is Insurance?

1.1. The Insurance Contract

1.2. The Insurance Policy

1.3. State Laws Governing Insurance

2. 2. Automobile Insurance

2.1. Laibility Coverage

2.2. Typical Provisions

2.3. "No-Fault" Insurance

2.4. Exclusions

3. 3. Insurance and Lawsuits

4. KEY-Click Circle

Comienza Ya. ¡Es Gratis!

Conéctate con Google

ó

Regístrate