NIC 2 INVENTARIOS

por GLADYS ESPINEL SUAREZ

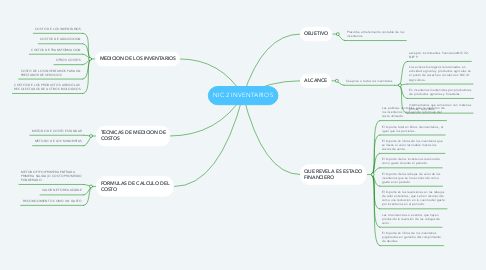

1. MEDICION DE LOS INVENTARIOS

1.1. COSTO DE LOS INVENTARIOS

1.2. COSTOS DE ADQUISICION

1.3. COSTOS DE TRANSFORMACION

1.4. OTROS COSTOS

1.5. COSTO DE LOS INVENTARIOS PARA UN PRESTADOR DE SERVICIOS

1.6. COSTOS DE LOS PRODUCTOS AGRICOLAS RECOLECTADOS DE ACTIVOS BIOLOGICOS

2. TECNICAS DE MEDICION DE COSTOS

2.1. METODO DE COSTO ESTANDAR

2.2. METODO DE LOS MINORISTAS

3. FORMULAS DE CALCULO DEL COSTO

3.1. METODO FIFO (PRIMERA ENTRADA PRIMERA SALIDA) O COSTO PROMEDIO PONDERADO.

3.2. VALOR NETO REALIZABLE

3.3. RECONOCIMIENTO COMO UN GASTO

4. OBJETIVO

4.1. Prescribe el tratamiento contable de los inventarios.

5. ALCANCE

5.1. Se aplica a todos los inventarios

5.1.1. excepto: instrumentos financierosNIC 32 - NIIF 9

5.1.2. Los activos biologicos relacionados en actividad agricola y productos agricolas en el punto de cosecha o recoleccion NIC 41 Agricultura.

5.1.3. En inventarios mantenidos por:productores de productos agricolas y forestales .

5.1.4. Intermediarios que comercian con materias primas cotizadas