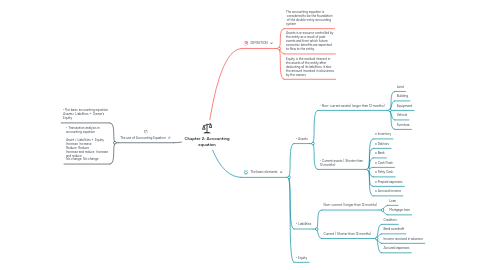

Chapter 2: Accounting equation

par Linh Phan

1. The use of Accounting Equation

1.1. •The basic accounting equation Assets= Liabilities + Owner’s Equity

1.2. • Transaction analysis in accounting equation Asset = Liabilities + Equity Increase Increase Reduce Reduce Increase and reduce Increase and reduce No change No change

2. DEFINITION

2.1. The accounting equation is considered to be the foundation of the double-entry accounting system

2.2. Assets is a resource controlled by the entity as a result of past events and from which future economic benefits are expected to flow to the entity.

2.3. Equity is the residual interest in the assets of the entity after deducting all its liabilities; it also the amount invested in a business by the owners

3. The basic elements

3.1. • Assets

3.1.1. - Non- current assets( longer than 12 months)

3.1.1.1. Land

3.1.1.2. Building

3.1.1.3. Equipment

3.1.1.4. Vehicle

3.1.1.5. Furniture

3.1.2. - Current assets ( Shorter than 12 months)

3.1.2.1. o Inventory

3.1.2.2. o Debtors

3.1.2.3. o Bank

3.1.2.4. o Cash Float

3.1.2.5. o Petty Cash

3.1.2.6. o Prepaid expenses

3.1.2.7. o Accrued income

3.2. • Liabilities

3.2.1. Non- current ( longer than 12 months)

3.2.1.1. Loan

3.2.1.2. Mortgage loan

3.2.2. Current ( Shorter than 12 months)

3.2.2.1. Creditors

3.2.2.2. Bank overdraft

3.2.2.3. Income received in advance

3.2.2.4. Accured expenses