Unlock the full potential of your projects.

Try MeisterTask for free.

Vous n'avez pas de compte ?

Inscription gratuite

Parcourir

Cartes en vedette

Catégories

Gestion de projet

Objectifs d'affaires

Ressources humaines

Brainstorming et analyse

Marketing et contenu

Éducation et remarques

Loisirs

Vie courante

Technologie

Design

Résumés

Autre

Langues

English

Deutsch

Français

Español

Português

Nederlands

Dansk

Русский

日本語

Italiano

简体中文

한국어

Autre

Montrer carte totale

Overview of VAT

Autre

LB

Laura Burrows

Suivre

Lancez-Vous.

C'est gratuit

S'inscrire avec Google

ou

s'inscrire

avec votre adresse e-mail

Cartes mentales similaires

Plan de carte mentale

Overview of VAT

par

Laura Burrows

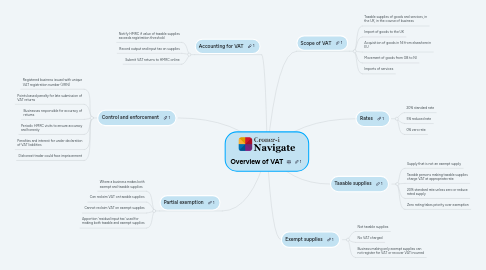

1. Accounting for VAT

1.1. Notify HMRC if value of taxable supplies exceeds registration threshold

1.2. Record output and input tax on supplies

1.3. Submit VAT returns to HMRC online

2. Control and enforcement

2.1. Registered business issued with unique VAT registration number (VRN)

2.2. Points based penalty for late submission of VAT returns

2.3. Businesses responsible for accuracy of returns

2.4. Periodic HMRC visits to ensure accuracy and honesty

2.5. Penalties and interest for under declaration of VAT liabilities

2.6. Dishonest trader could face imprisonment

3. Partial exemption

3.1. Where a business makes both exempt and taxable supplies

3.2. Can reclaim VAT on taxable supplies

3.3. Cannot reclaim VAT on exempt supplies

3.4. Apportion 'residual input tax' used for making both taxable and exempt supplies

4. Scope of VAT

4.1. Taxable supplies of goods and services, in the UK, in the course of business

4.2. Import of goods to the UK

4.3. Acquisition of goods in NI from elsewhere in EU

4.4. Movement of goods from GB to NI

4.5. Imports of services

5. Rates

5.1. 20% standard rate

5.2. 5% reduced rate

5.3. 0% zero rate

6. Exempt supplies

6.1. Not taxable supplies

6.2. No VAT charged

6.3. Business making only exempt supplies can not register for VAT or recover VAT incurred

7. Taxable supplies

7.1. Supply that is not an exempt supply

7.2. Taxable persons making taxable supplies charge VAT at appropriate rate

7.3. 20% standard rate unless zero or reduce rated supply

7.4. Zero rating takes priority over exemption

Lancez-vous. C'est gratuit!

Connectez-vous avec Google

ou

S'inscrire