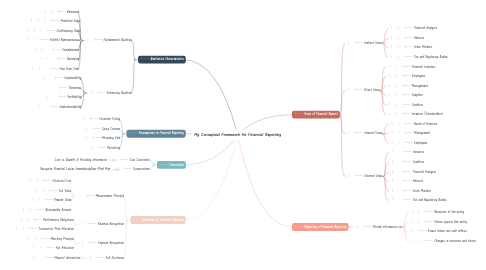

1. ├── **Users of Financial Reports**

1.1. │ ├── Indirect Users

1.1.1. │ │ ├── Financial Analysts

1.1.2. │ │ ├── Advisors

1.1.3. │ │ ├── Stock Markets

1.1.4. │ │ └── Tax and Regulatory Bodies

1.2. │ ├── Direct Users

1.2.1. │ │ ├── Potential Investors

1.2.2. │ │ ├── Employees

1.2.3. │ │ ├── Management

1.2.4. │ │ ├── Suppliers

1.2.5. │ │ └── Creditors

1.2.6. │ │ ├── Investors (Shareholders)

1.3. │ ├── Internal Users

1.3.1. │ │ ├── Board of Directors

1.3.2. │ │ ├── Management

1.3.3. │ │ └── Employees

1.4. │ └── External Users

1.4.1. │ ├── Investors

1.4.2. │ ├── Creditors

1.4.3. │ ├── Financial Analysts

1.4.4. │ ├── Advisors

1.4.5. │ ├── Stock Markets

1.4.6. │ └── Tax and Regulatory Bodies

2. ├── **Objectives of Financial Reporting**

2.1. │ ├── Provide information on:

2.1.1. │ │ ├── Resources of the entity

2.1.2. │ │ ├── Claims against the entity

2.1.3. │ └── Assess future net cash inflows

2.1.4. │ │ └── Changes in resources and claims

3. ├── **Qualitative Characteristics**

3.1. │ ├── Fundamental Qualities

3.1.1. │ │ ├── Relevance

3.1.2. │ │ │ ├── Predictive Value

3.1.3. │ │ │ └── Confirmatory Value

3.1.4. │ │ └── Faithful Representation

3.1.5. │ │ ├── Completeness

3.1.6. │ │ ├── Neutrality

3.1.7. │ │ └── Free from Error

3.2. │ └── Enhancing Qualities

3.2.1. │ ├── Comparability

3.2.2. │ ├── Timeliness

3.2.3. │ ├── Verifiability

3.2.4. │ └── Understandability

4. ├── **Assumptions in Financial Reporting**

4.1. │ ├── Economic Entity

4.2. │ ├── Going Concern

4.3. │ ├── Monetary Unit

4.4. │ └── Periodicity

5. └── **Constraints**

5.1. ├── Cost Constraint

5.1.1. Cost vs. Benefit of Providing Information

5.2. └── Conservatism

5.2.1. Recognize Potential Losses ImmediatelyNew Mind Map

6. ├── **Principles of Financial Reporting**

6.1. │ ├── Measurement Principle

6.1.1. │ │ ├── Historical Cost

6.1.2. │ │ ├── Fair Value

6.1.3. │ │ ├── Present Value

6.1.4. │ │ └── Recoverable Amount

6.2. │ ├── Revenue Recognition

6.2.1. │ │ ├── Performance Obligations

6.2.2. │ │ └── Transaction Price Allocation

6.3. │ ├── Expense Recognition

6.3.1. │ │ ├── Matching Principle

6.3.2. │ │ └── Fair Allocation

6.4. │ └── Full Disclosure

6.4.1. │ └── Material Information