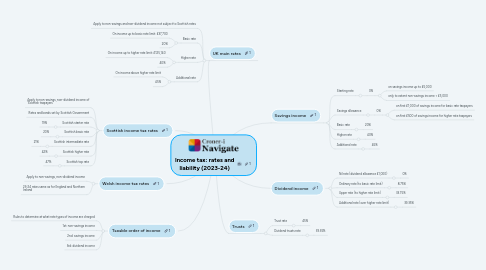

Income tax: rates and liability (2023-24)

Julia Bowyerにより

1. UK main rates

1.1. Apply to non-savings and non-dividend income not subject to Scottish rates

1.2. Basic rate

1.2.1. On income up to basic rate limit: £37,700

1.2.2. 20%

1.3. Higher rate

1.3.1. On income up to higher rate limit: £125,140

1.3.2. 40%

1.4. Additional rate

1.4.1. On income above higher rate limit

1.4.2. 45%

2. Scottish income tax rates

2.1. Apply to non-savings, non-dividend income of 'Scottish taxpayers'

2.2. Rates and bands set by Scottish Government

2.3. Scottish starter rate

2.3.1. 19%

2.4. Scottish basic rate

2.4.1. 20%

2.5. Scottish intermediate rate

2.5.1. 21%

2.6. Scottish higher rate

2.6.1. 42%

2.7. Scottish top rate

2.7.1. 47%

3. Taxable order of income

3.1. Rules to determine at what rate types of income are charged

3.2. 1st: non-savings income

3.3. 2nd: savings income

3.4. 3rd: dividend income

4. Welsh income tax rates

4.1. Apply to non-savings, non-dividend income

4.2. 23-24 rates same as for England and Northern Ireland

5. Savings income

5.1. Starting rate

5.1.1. 0%

5.1.1.1. on savings income up to £5,000

5.1.1.2. only to extent non-savings income < £5,000

5.2. Savings allowance

5.2.1. 0%

5.2.1.1. on first £1,000 of savings income for basic rate taxpayers

5.2.1.2. on first £500 of savings income for higher rate taxpayers

5.3. Basic rate

5.3.1. 20%

5.4. Higher rate

5.4.1. 40%

5.5. Additional rate

5.5.1. 45%

6. Dividend income

6.1. Nil rate (dividend allowance £1,000)

6.1.1. 0%

6.2. Ordinary rate (to basic rate limit)

6.2.1. 8.75%

6.3. Upper rate (to higher rate limit)

6.3.1. 33.75%

6.4. Additional rate (over higher rate limit)

6.4.1. 39.35%

7. Trusts

7.1. Trust rate

7.1.1. 45%

7.2. Dividend trusts rate

7.2.1. 39.35%