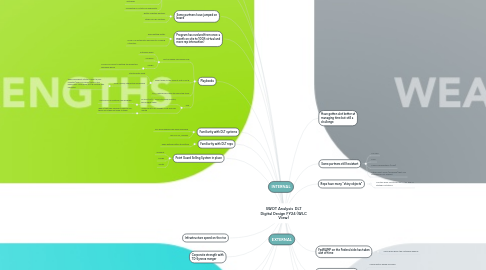

1. Proven track record

1.1. Measurable

1.1.1. WLC has contributed at least $1M in net margin (including billings to DLT)

1.1.2. ROI for the program: 260%

1.2. Intangible

1.2.1. Coaching and mentoring reps

1.2.1.1. A value add for partners

1.2.2. Much faster ramp up for new reps

1.2.3. Proposal templates are commonly used across SLED and FED-- have driven many sales beyond what is tracked in Smart

1.2.4. Good partnership and reputation at Autodesk

1.2.5. Cemented DLT status as aggregator

2. Some partners have jumped on board

2.1. Better Together partners

2.2. Other Non-BT partners

3. Program has evolved from once a month on site to 100% virtual and more rep interaction)

3.1. Reps getting better

3.2. More of a systematic approach to covering a territory

4. Playbooks

4.1. Part of regular call blocks now

4.1.1. Autodesk plays

4.1.2. Archibus

4.1.3. Aurigo

4.1.3.1. ISP will be crucial to getting the Essentials campaign going

4.2. Wasnt even on the radar at first in 2018

4.2.1. Started with Word

4.2.2. Now a visual, interactive experience

4.2.2.1. Reps have spent a total of over 15,000 minutes (over 240 hours) total in the playbooks--only rolled out 18 months ago officially!

4.3. DLT, channel reps have the same talk track

4.4. Use

4.4.1. As of 9/24/21- 3200 total view minutes, 935 unique views

4.4.1.1. Not bad for a relatively new program

4.4.2. Comes out to an average of an hour per month

4.4.2.1. Idea is that they shouldn't need to use them once they get used to them

5. Familiarity with DLT systems

5.1. DLT Email address has been invaluable

5.2. Use of CJIS, GovWin

6. Familiarity with DLT reps

6.1. Reps getting better at huntting

7. Point Guard Selling System in place

7.1. Archibus

7.2. Aurigo

7.3. Avuity

8. INTERNAL

9. EXTERNAL

10. Have gotten alot better at managing time but still a challenge

11. Hunters now report into DD

11.1. Turnover but seems to have a good team now

12. Some partners still hesistant

12.1. US CAD

12.2. ASTI

12.3. CADD Microsystems (SLED)

12.4. Others don't know (somehow) that I am available for call support

13. Reps have many "shiny objects"

13.1. Monthly goals sometimes get in the way of strategic initiatives

14. FedRAMP on the Federal side has taken alot of time

14.1. Some hope given the Autodesk webinar

15. Autodesk seems to be inching into the direct deal space

15.1. Consumption based licensing

15.2. PlanGrid

15.3. Innovyze

15.4. Aurigo Masterworks

16. Competitors

16.1. Trimble

16.1.1. TBC

16.1.2. E Builder/ Cityworks

16.2. Bentley

16.2.1. SLED- State DOTs

16.2.2. FED- USACE, IMCOM, USDOT